Index >> Business >> Investment Tools >> WebCab Portfolio for .NET

Report SpywareWebCab Portfolio for .NET 4.2

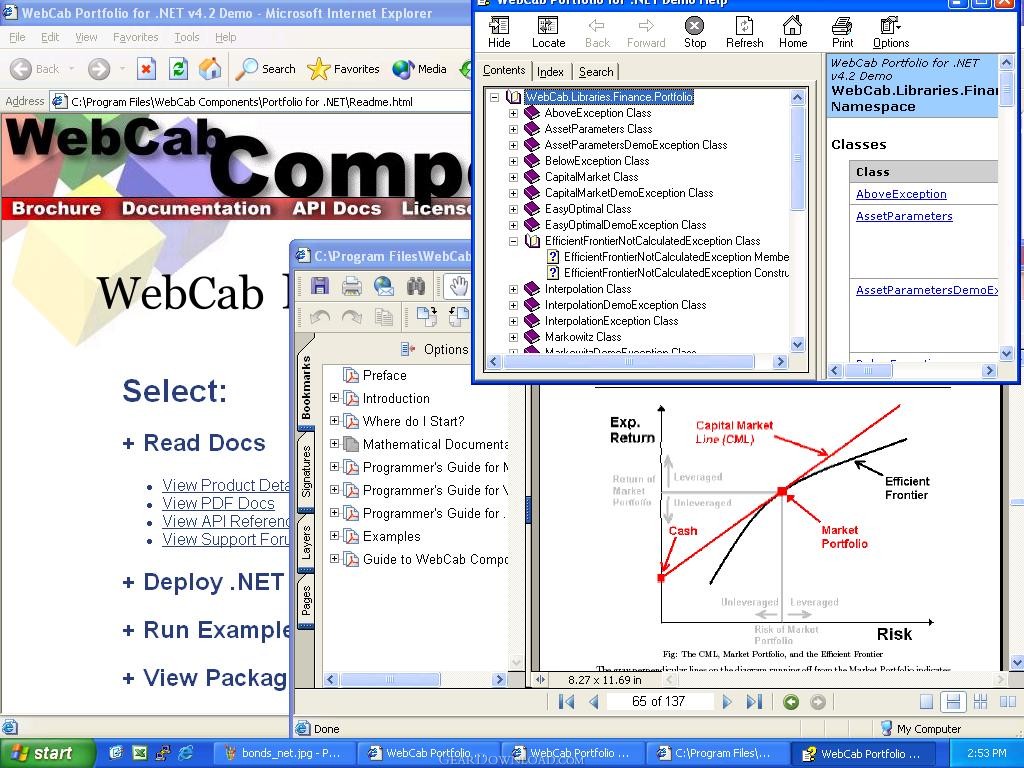

Click to enlarge screenshot

Click to enlarge screenshot

Software Description:

WebCab Portfolio for .NET - .NET, COM and Web service implementation of the Markowitz Theory and CAPM.

.NET, COM and XML Web service implementation of Markowitz Theory and Capital Asset Pricing Model (CAPM) to analyze and construct the optimal portfolio with/without asset weight constraints with respect to Markowitz Theory by giving the risk, return or investors utility function; or with respect to CAPM by given the risk, return or Market Portfolio weighting. Also includes Performance Evaluation, extensive auxiliary classes/methods including equation solve and interpolation procedures, analysis of Efficient Frontier, Market Portfolio and CML.

Utility Functionality included:

Interpolation - Cubic spline and general polynomial interpolation procedures to assist in the study of the Efficient Frontier

SolveFrontier - Solve the Efficient Frontier with respect to the risk, return, or the investors utility function.

MaxRange - Maximum range of the constrained Efficient Frontier

AssetParameters - Evaluation of the covariance matrix, expected return, volatility, portfolio risk/variance.

Performance Evaluation - Offers a number of procedures for accessing the return and risk adjusted return (Treynors Measure, Sharpes Ratio).

This product also has the following technology aspects:

3-in-1: .NET, COM, and XML Web services - Three DLLs, Three API Docs, Three Sets of Client Example all in 1 product. Offering a 1st class .NET, COM, and XML Web service product implementation.

Extensive Client Examples - Multiple client examples including .NET (C#, VB.NET, C++.NET), COM and XML Web services (C#, VB.NET)

ADO Mediator - The ADO Mediator assists the .NET developer in writing DBMS enabled applications by transparently combining the financial and mathematical functionality of our .NET components with the ADO.NET Database Connectivity model.

Compatible Containers - Visual Studio 6, Visual Studio .NET, Borland's C++ Builder, Borland Delphi 3 - 2005, Office 97/2000/XP/2003

ASP.NET Web Application Examples

ASP.NET Examples with Synthetic ADO.NET

TAGS: .NET, C#, C++

.NET, COM and XML Web service implementation of Markowitz Theory and Capital Asset Pricing Model (CAPM) to analyze and construct the optimal portfolio with/without asset weight constraints with respect to Markowitz Theory by giving the risk, return or investors utility function; or with respect to CAPM by given the risk, return or Market Portfolio weighting. Also includes Performance Evaluation, extensive auxiliary classes/methods including equation solve and interpolation procedures, analysis of Efficient Frontier, Market Portfolio and CML.

Utility Functionality included:

Interpolation - Cubic spline and general polynomial interpolation procedures to assist in the study of the Efficient Frontier

SolveFrontier - Solve the Efficient Frontier with respect to the risk, return, or the investors utility function.

MaxRange - Maximum range of the constrained Efficient Frontier

AssetParameters - Evaluation of the covariance matrix, expected return, volatility, portfolio risk/variance.

Performance Evaluation - Offers a number of procedures for accessing the return and risk adjusted return (Treynors Measure, Sharpes Ratio).

This product also has the following technology aspects:

3-in-1: .NET, COM, and XML Web services - Three DLLs, Three API Docs, Three Sets of Client Example all in 1 product. Offering a 1st class .NET, COM, and XML Web service product implementation.

Extensive Client Examples - Multiple client examples including .NET (C#, VB.NET, C++.NET), COM and XML Web services (C#, VB.NET)

ADO Mediator - The ADO Mediator assists the .NET developer in writing DBMS enabled applications by transparently combining the financial and mathematical functionality of our .NET components with the ADO.NET Database Connectivity model.

Compatible Containers - Visual Studio 6, Visual Studio .NET, Borland's C++ Builder, Borland Delphi 3 - 2005, Office 97/2000/XP/2003

ASP.NET Web Application Examples

ASP.NET Examples with Synthetic ADO.NET

TAGS: .NET, C#, C++

100% Clean:

WebCab Portfolio for .NET 4.2 is 100% clean

WebCab Portfolio for .NET 4.2 is 100% cleanThis download (WebCabPortfolioDemoNETService.Msi) was tested thoroughly and was found 100% clean. Click "Report Spyware" link on the top if you found this software contains any form of malware, including but not limited to: spyware, viruses, trojans and backdoors.

Related Software:

- Discounted Cash Flow Analysis Calculator 2.1 - Discounted Cash Flow Analysis of 14 cash flow series with 5 discount rates.

- Visual Options Analyzer 4.5.2 - Visual Stock Options Analyzer. Build options strategies, hedging.

- AnalyzerXL 6.1.37 - Technical analysis, stock quotes, investment portfolio in Microsoft Excel

- TraderXL Pro Package 6.1.39 - All-in-one investment solution for Microsoft Excel

- Portfolio Performance Monitoring 3.0 - Monitoring and tracking the performance of a portfolio of financial assets.

- Investment and Business Valuation 3.0 - Evaluating a wide range of investment proposal and business valuation scenarios.

- GoldenGem 1.4 - Goldengem is one of the best neural net stock market programs.

- Parity Plus - Stock Charting and Technical Analysi 2.1 - Parity Plus is one of the most powerful Stock Charting and Technical Analysis Pr

- DataBull 6.2.6 - DataBull downloads stockquotes into any technical analysis software program.

- Options Czar 2.0 - Free Options Strategy Management Software

top 10 most downloaded

recommended software

-

- A VIP Organizer

- VIP Organizer is a time and task management software which uses To Do List method to help you get through more work spending less time. It increases y...

-

- Salon Calendar

- Salon Calendar is a software tool designed specially for hair salons, beauty, manicure or aesthetic shops, tanning salons, fitness studios, wedding sa...