Index >> Business >> Investment Tools >> WebCab Options and Futures for .NET

Report SpywareWebCab Options and Futures for .NET 3.0

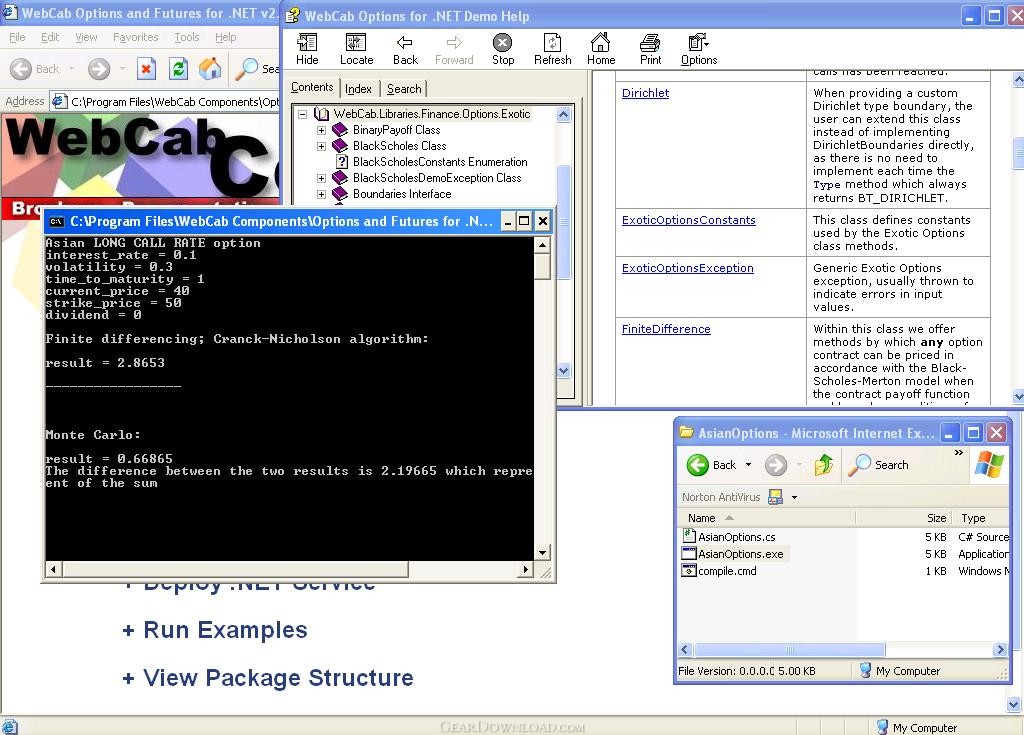

Click to enlarge screenshot

Click to enlarge screenshot

Software Description:

WebCab Options and Futures for .NET - Add our Equity derivatives pricing framework to COM, .NET and Web service Apps

3-in-1: .NET, COM and XML Web service Components for pricing option and futures contracts using Monte Carlo and Finite Difference techniques. General Monte Carlo pricing framework: wide range of contracts, price, interest and vol models. Price European, Asian, American, Lookback, Bermuda and Binary Options using Analytic, Monte Carlo and Finite Difference in accordance with a number of vol, price, volatility and rate models.

General Pricing Framework offers the following predefined Models and Contracts:

Contracts: Asian Option, Binary Option, Cap, Coupon Bond, Floor, Forward Start stock option, Lookback Option, Ladder Option, Vanilla Swap, Vanilla Stock Option, Zero Coupon Bond, Barrier Option, Parisian Option, Parasian Option, Forward and Future.

Interest Rate Models: Constant Spot Rate, Constant (in time) Yield curve, One factor stochastic models (Vasicek, Black-Derman-Toty (BDT), Ho & Lee, Hull and White), Two factor stochastic models (Breman & Schwartz, Fong & Vasicek, Longstaff & Schwartz), Cox-Ingersoll-Ross Equilibrium model, Spot rate model with automatic yield (Ho & Lee, Hull & White), Heath-Jarrow-Morton forward rate model, Brace-Gatarek-Musiela (BGM) LIBOR market model.

Price Models: Constant price model, General deterministic price model, Lognormal price model, Poisson price model.

Volatility Models: Constant Volatility Models, General Deterministic Volatility model, Hull & White Stochastic model of the Variance, Hoston Stochastic Volatility model.

Monte Carlo Princing Engine: Evaluate price estimate accordance to number of iterations or maximum expected error. Evaluate the standard deviation of the price estimate, and the minimum/maximum expected price for a given confidence level.

This product also has the following technology aspects:

3-in-1: .NET, COM, and XML Web services - 3 DLLs, 3 API Docs,...

Extensive Client Examples (C#, VB, C++,..)

ADO Mediator

Compatible Containers (VS, VS.NET, Office, C++Builder, Delphi)

Limitations: 50 Uses Trial

TAGS: .NET, C#, American, Binary

3-in-1: .NET, COM and XML Web service Components for pricing option and futures contracts using Monte Carlo and Finite Difference techniques. General Monte Carlo pricing framework: wide range of contracts, price, interest and vol models. Price European, Asian, American, Lookback, Bermuda and Binary Options using Analytic, Monte Carlo and Finite Difference in accordance with a number of vol, price, volatility and rate models.

General Pricing Framework offers the following predefined Models and Contracts:

Contracts: Asian Option, Binary Option, Cap, Coupon Bond, Floor, Forward Start stock option, Lookback Option, Ladder Option, Vanilla Swap, Vanilla Stock Option, Zero Coupon Bond, Barrier Option, Parisian Option, Parasian Option, Forward and Future.

Interest Rate Models: Constant Spot Rate, Constant (in time) Yield curve, One factor stochastic models (Vasicek, Black-Derman-Toty (BDT), Ho & Lee, Hull and White), Two factor stochastic models (Breman & Schwartz, Fong & Vasicek, Longstaff & Schwartz), Cox-Ingersoll-Ross Equilibrium model, Spot rate model with automatic yield (Ho & Lee, Hull & White), Heath-Jarrow-Morton forward rate model, Brace-Gatarek-Musiela (BGM) LIBOR market model.

Price Models: Constant price model, General deterministic price model, Lognormal price model, Poisson price model.

Volatility Models: Constant Volatility Models, General Deterministic Volatility model, Hull & White Stochastic model of the Variance, Hoston Stochastic Volatility model.

Monte Carlo Princing Engine: Evaluate price estimate accordance to number of iterations or maximum expected error. Evaluate the standard deviation of the price estimate, and the minimum/maximum expected price for a given confidence level.

This product also has the following technology aspects:

3-in-1: .NET, COM, and XML Web services - 3 DLLs, 3 API Docs,...

Extensive Client Examples (C#, VB, C++,..)

ADO Mediator

Compatible Containers (VS, VS.NET, Office, C++Builder, Delphi)

Limitations: 50 Uses Trial

TAGS: .NET, C#, American, Binary

100% Clean:

WebCab Options and Futures for .NET 3.0 is 100% clean

WebCab Options and Futures for .NET 3.0 is 100% cleanThis download (WebCabOptionsDemoNETService.zip) was tested thoroughly and was found 100% clean. Click "Report Spyware" link on the top if you found this software contains any form of malware, including but not limited to: spyware, viruses, trojans and backdoors.

Related Software:

- Discounted Cash Flow Analysis Calculator 2.1 - Discounted Cash Flow Analysis of 14 cash flow series with 5 discount rates.

- Visual Options Analyzer 4.5.2 - Visual Stock Options Analyzer. Build options strategies, hedging.

- AnalyzerXL 6.1.37 - Technical analysis, stock quotes, investment portfolio in Microsoft Excel

- TraderXL Pro Package 6.1.39 - All-in-one investment solution for Microsoft Excel

- Portfolio Performance Monitoring 3.0 - Monitoring and tracking the performance of a portfolio of financial assets.

- Investment and Business Valuation 3.0 - Evaluating a wide range of investment proposal and business valuation scenarios.

- GoldenGem 1.4 - Goldengem is one of the best neural net stock market programs.

- Parity Plus - Stock Charting and Technical Analysi 2.1 - Parity Plus is one of the most powerful Stock Charting and Technical Analysis Pr

- DataBull 6.2.6 - DataBull downloads stockquotes into any technical analysis software program.

- Options Czar 2.0 - Free Options Strategy Management Software

top 10 most downloaded

recommended software

-

- A VIP Organizer

- VIP Organizer is a time and task management software which uses To Do List method to help you get through more work spending less time. It increases y...

-

- Salon Calendar

- Salon Calendar is a software tool designed specially for hair salons, beauty, manicure or aesthetic shops, tanning salons, fitness studios, wedding sa...